A leveraged IRR calculation (or levered IRR) is required when evaluating a commercial property investment or a residential property in which the investor intends to mortgage financing in order to borrow a percentage of the money required to acquire the property under consideration. The leveraged IRR analysis incorporates the mortgage payments for the repayment of the loan and thus, the latest mortgage rate forecast is very important for commercial property investment analysis.

A leveraged IRR calculation, therefore, uses the discounted cash flow model (DCF) and takes into account, in addition to the cost and revenue items taken into account in an unleveraged IRR analysis, the debt service payments to service the loan over the holding period, as well as the repayment of the remaining loan balance upon the sale of the property. Furthermore, it takes into account any taxable income deductions that the owner may be entitled due to interest payments for the loan.

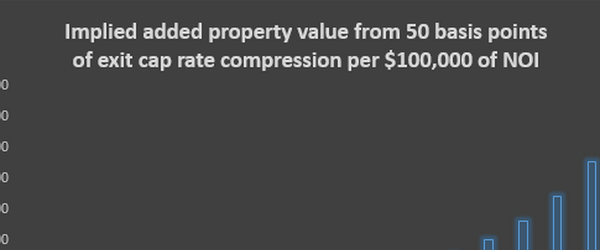

One of the significant unknowns in the leveraged IRR (and the unleveraged IRR) calculation is the resale price of the property under consideration at the end of the holding period. The most commonly used technique for the estimation of this resale value is the forecast of an exit cap rate which is applied to the net operating income (NOI) of the last year of the holding period. The exact formula applied is:

Terminal Value = NOI/Exit Cap Rate

Usually the assumed exit or terminal cap rate is higher than the entry cap rate in order to reflect the uncertainty of future cash flows. The entry or going-in cap rate is calculated as the ratio of acquisition price over the property’s actual NOI at the time of the purchase.

Making reasonable assumptions in the leveraged IRR calculation is of critical importance for making successful property investments. The leveraged IRR calculation over a holding period is not an easy task, especially for multi-tenant properties, as it is predicated on the correct calculation of expected cash flow for each year taking into account all relevant revenues and expenses. In this sense it requires lots of number crunching. For this reason there are several property investment analysis software programs that can make this task much easier and more automated and can help avoid mistakes.

Problems Of Leveraged IRR Calculation

One of the potentially problematic assumptions of the leveraged IRR calculation is the reinvestment assumption. In other words, the leveraged IRR calculation formula incorporates the assumption that all positive cash flows in any period are reinvested at the same rate as the calculated IRR. For example, an estimated IRR of 150% implies the expectation that all positive cash flows received at any period will be re-invested immediately at a rate of return of 150%. However, this assumption maybe very unrealistic if the investor does not have immediately available investment vehicles that will be providing a 150% return upon investment of the money. If the actual reinvestment rate of received cash flow is considerably lower then the true return of the investment will be considerably lower.

Another potential problem of the leveraged IRR calculation is the multiple-solutions problem. This problem is more likely to appear when the income stream that is used for the calculation of the IRR has sign reversals, that is, cash flow switches from positive to negative and vice versa. Greer and Farrell (1992) suggest that in such a case there may be as many IRR solutions as the number of sign reversals.

Modified IRR Calculation

If the investor feels that he/she cannot reinvest all positive cash flows immediately as they are received at an immediately accruing rate of return equal to the estimated IRR then the leveraged IRR calculation needs to use the so called a Modified IRR» (MIRR) formula, which takes into account that all positive cash flows are reinvested at a different rate than the IRR of the investment analysed. The MIRR allows you to enter a different reinvestment rate that is applied to the property’s annual cash flow. The rate used is generally a savings rate or a government bond rate. The return estimated using the MIRR formula, more closely reflects reality as it is rarely possible to reinvest the cash flow from a particular project at the same exact rate of return, which is derived using the IRR formula.

The MIRR calculation involves the following three steps:

1. Find the present value of negative cash flows incurred in any year during the course of the investment, discounting them at the annual interest rate that you would pay to cover any negative cash flows incurred during the life of the investment (finance rate). 2. Calculate the future value of positive cash flows incurred in any year during the holding period of the investment, by growing them at the interest rate expected to be earned on cash generated by the investment (Reinvestment Rate). This re-investment rate can be the government bond rate, or another rate depending on each investor’s availability of immediately available investment opportunities.

3. Calculate the average interest rate that grows the adjusted investment as calculated in step 1 into the adjusted amount as calculated in step 2

Comments